February 24, 2022

Alpine Macro Corporate Bond Allocation Calls

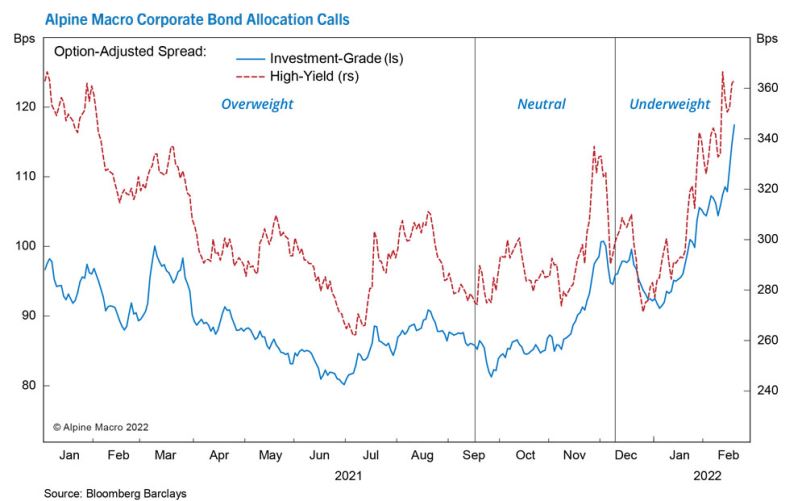

Our U.S. Bond Strategy service gradually transitioned last year from aggressively overweight to underweight in corporate bonds. This recommendation proved to be opportune, at a time when the consensus believed that healthy corporate profits, economic momentum and a vanishingly low default rate would keep the sector well bid. Spreads have widened sharply this year, but we believe that credit is still not priced for the coming mean-reversion in defaults in 2022. Find out more in this report.