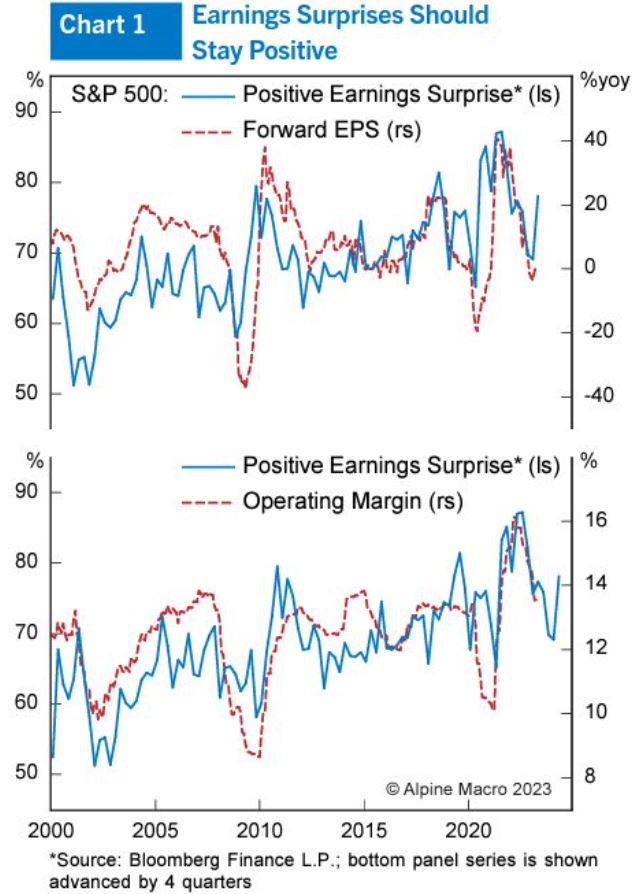

What Will Drive Equities: Positive EPS Surprises Or Looming Recession?

The Chart shows that earnings surprises, which lead forward EPS, rose sharply in Q1. Is this sustainable as the economy slows, the #creditcrunch intensifies, and Fed rate hikes have a lagged impact on demand? Cost inflation trends will be critical.

David Abramson

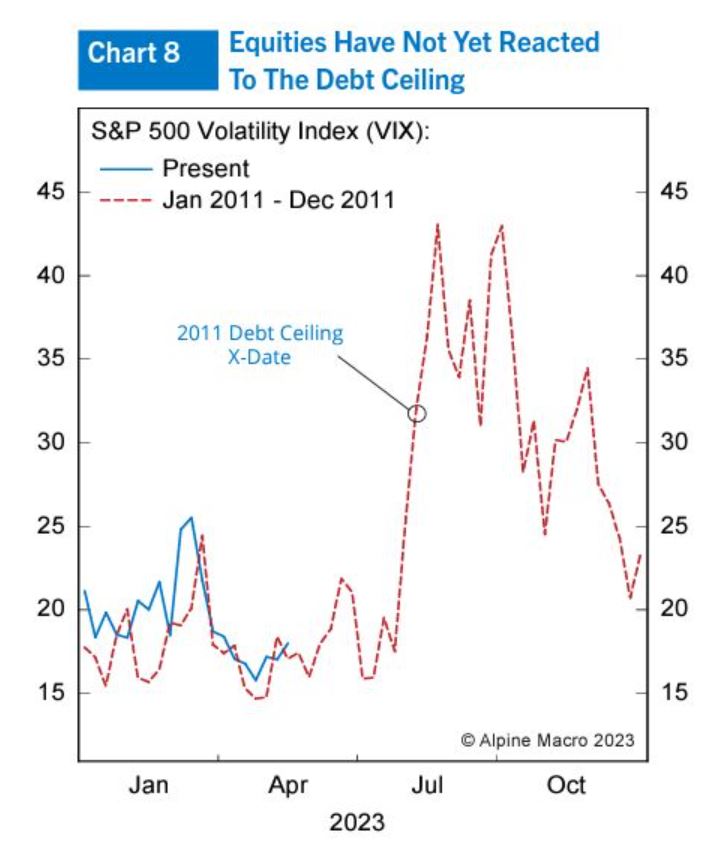

The Debt Ceiling Drama Unfolds!

As the debtceiling deadline nears, does deeper market volatility loom? Which way will equities and Treasuries move? Will history repeat itself with a 2011-style crisis, or will the current policymaking gridlock take another course? Ultimately, will Congress manage to pass legislation right before the X-Date, avoiding a debt ceiling breach?

Chen Zhao

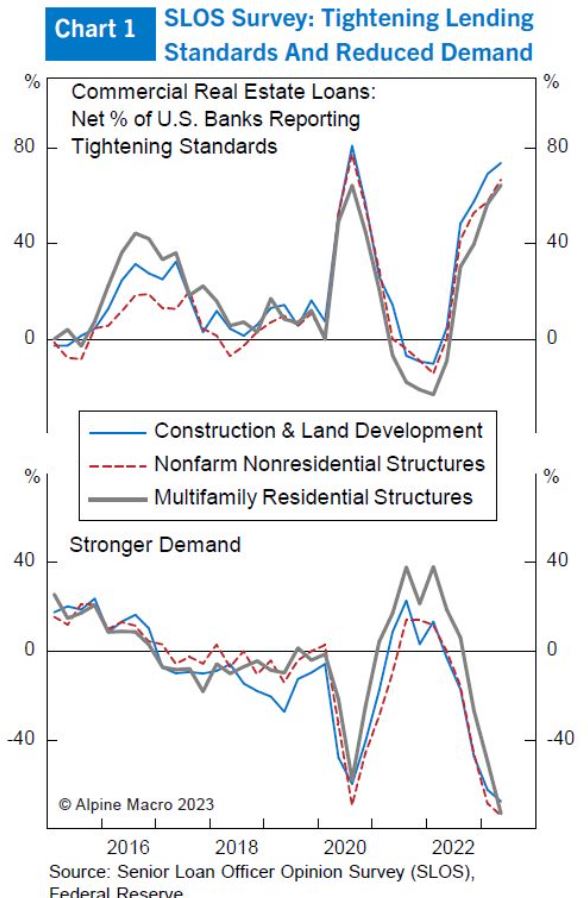

Commercial Real Estate: Different This Time?

The #CRE sector looks headed for a brutal downward adjustment, judging from ominous remarks by both the Fed and well-respected #money managers, not to mention the dire Q1 Fed Senior Loan Officers Survey (see Chart). But is all that gloom warranted? The contrarian bullish side to the story provides specific investment opportunities resulting from violent dislocation in the sector.

David Abramson

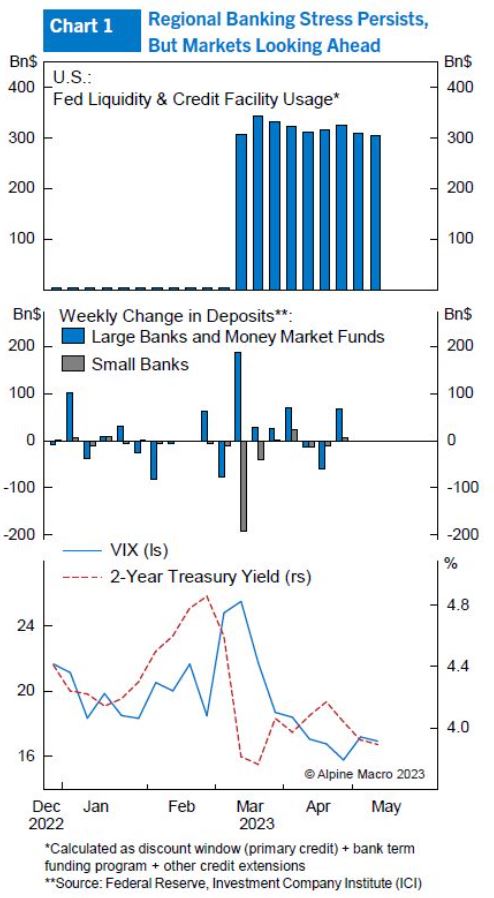

Intensifying Credit Crunch

The Chart shows that usage of the three #Fed emergency facilities remains high and the flight to quality persists. Yet small #bank deposit outflows are slowing. Stock and bond markets are calm. Is the crisis at a late stage or will the #credit crunch intensify, forcing the Fed to back off?

David Abramson

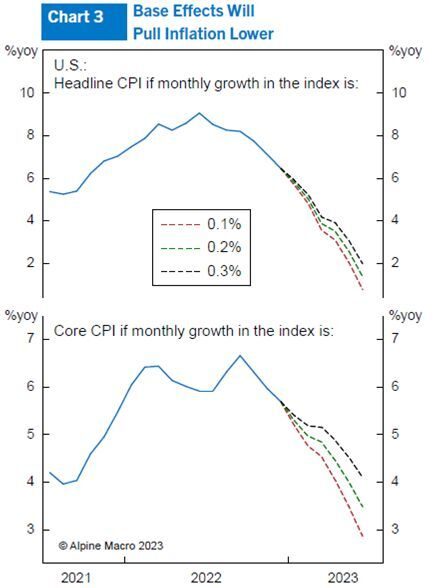

Base Effects Will Pull Inflation Lower

The risk/reward balance for relative-return bond investors is quite different from those interested in total return.

Mark McClellan